Buying Gold Stocks With Hedges On The GLD. A 2025 Playbook.

Gold is breaking new highs under the radar and I am buying despite what Buffett says.

One interesting note before I start. Gold stocks have historically traded at very high valuations. I could not wrap my head around the valuations when gold was below $2000. Now that valuations are much more reasonable there does not seem to be much enthusiasm.

Did gold bugs move to Bitcoin? Were they just herd buyers disguising themselves as precious metal experts? I don’t know. But the lack of attention gold is getting while breaking new highs is creating opportunities.

The bears could argue that costs are rising for most gold producers because of inflation, higher royalty payments, more difficulty finding reserves etc.. The counter argument would be the move in gold has risen much faster than these cost increases. And higher costs would also be a barrier for new entrants or new mines coming online which would lower supply and increase prices.

Before I get into my hedge trade I want to provide an update on IMG and go over a couple of other names and their valuations.

Update on IMG

I wrote an article on IMG earlier linked below.

Iamgold: Is the market pricing this stock correctly? A bet based on probabilities.

I am not an expert in gold production, I am a generalist investor. If you ask me about the technical aspects of getting a gold mine running I’d tell you I don’t know. But that is not the goal of an investor. Most of the work is assessing risk and position sizing based on what you know.

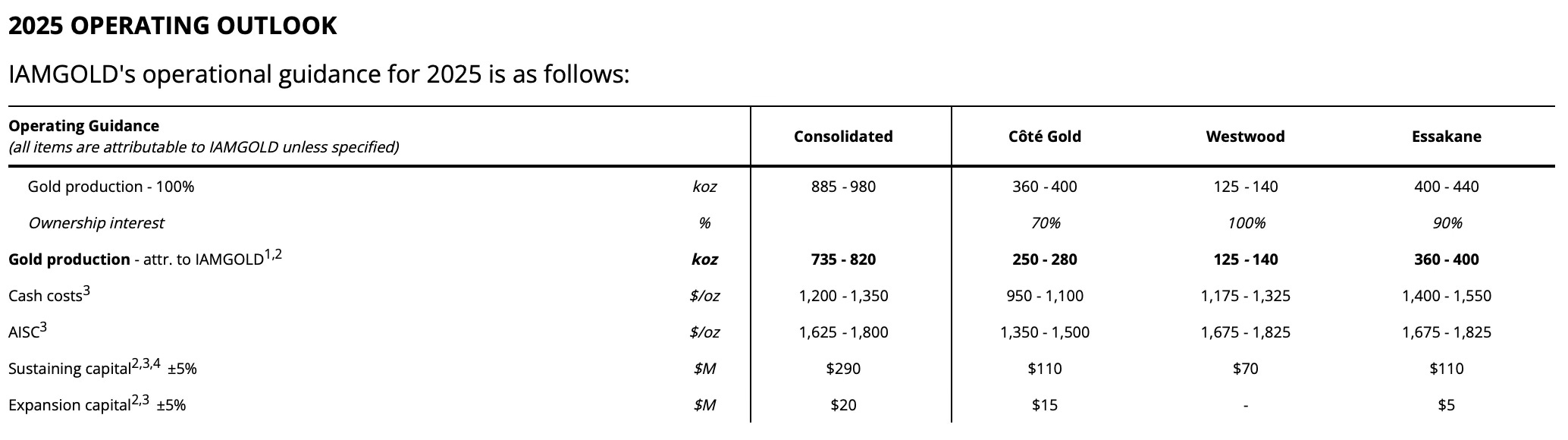

Some updates from the latest release. The bad news first. Cote will not ramp up to full production based on their 2025 outlook. And expenses at their Esakane mine will be higher next year as noted below.

And the market might be pricing more risk with their Esakane mine because of the issues Barrick Gold had at their Mali mines. But recent developments show that Barrick has resumed negotiations with the Mali government over mine disputes, so this might dissipate fears with investors.

Now for the good news. Iamgold hit full capacity throughput in a couple months in Q4. And 2025 mid-point guidance is at about 84% of capacity which is not too bad.

At $2500 gold prices I estimate they can generate about $285M at their Cote mine (no tax is expected to be paid for Cote profits in the first 6 years of production), $99M from Westwood, and about $200M from Essakane (after-tax using a rate of 30%).

In total that is about $584M USD in free cash flow on a current market cap of $3.4B USD for their US listed shares (IAG). They have $900M in debt denominated in Canadian dollars, which is pretty low and could be paid off fairly quickly. Though as noted in my the article there are risks, especially with the Essakane mine as noted above. Though the risk with the Cote mine seems to have decreased.

One obvious risk is the price of gold. When I opened my position I added puts in the GLD trust ETF at $2500 in case prices drop next year. Note also that in the above FCF calculation I used $2500 for my estimates but gold is currently sitting above $2700.

Gold company valuations

I was looking through an article posted by Value Degen’s Substack and he noted Endeavour mining so I decided to do a little more research. The company had an interesting slide in their presentation which I included below.

It shows the production volume and the all-in sustaining costs of several gold mining. So I looked at the valuations of several producers based on production volume to AISC to where the stock is trading. I already own Iamgold but I added exposure to a couple of new names. Newmont mining which has lower jurisdiction risk and Endeavour mining which operates in higher risk areas.

Newmont Mining NEM

For Newmont if they produce 7 million oz of gold in 2025 I am calculating $5B USD in EBIT using $1600 in AISC at $2500 gold prices. This includes about $330M in growth capital spending. Then you have ~$320 in interest expense and a 33% effective tax rate. So net FCF of about $3.1 Billion.

Every $100 increase in margins from lower AISC or higher gold prices nets about an additional $470M in after tax earnings.

With a market cap of $47B USD at $2500 gold the FCF multiple is 15. At $2700 this drops to just under 12.

Their net debt is only $6B which is low compared to the FCF they can generate. They also plan on returning capital to shareholders. Note that they also sell copper, silver etc. so you can add a couple hundred million to FCF but I did not include it in my calculation because it is not too material and this is mostly a play on gold.

The good thing about Newmont is they have mines in lower risk jurisdictions so it takes headline risk off the table.

Endeavour Mining EDVMF

So this one is more risky. All their mines are in Africa and as noted above with Barrick Gold this creates both perceived risks and real risks. Quantifying this risk is difficult but it looks like it is already priced into the stock. Their AISC to production volume in comparison to where the stock is trading provides pretty significant upside if they can maintain production and keep good relations in the countries they operate.

Just to put it into perspective their US listed shares trade at a market cap of $4.65B. Their all-in sustaining costs are listed as $1250. They also list non-sustaining costs of roughly $200M although their presentation does not specificy whether this is included in their AISC so I am adding it to total costs to be conservative in my estimates. They are guiding for minimal growth capital for 2025. So margins are $1050 per oz of production. At gold prices of $2500 and with production of 1.1M oz per year, total pre-tax income is $1.15B USD. Their tax rate is about 27% so after tax profits will be about $840M.

That is a 5.5 FCF multiple on the market cap.

And they only have about $700M of long term debt and $470M drawn on their revolver. Interest payments would be roughly only $50M per year.

Gold price and gold equities trade

I wrote a bunch of stuff below, if you don’t want to read the details here is the big picture trade. A small position in your portfolio, say 2% where you buy a small basket of gold stocks to diversify your risk in specific gold names (you can even buy the GDX or the GDXJ, while adding hedges on the price of gold through the GLD trust ETF.

The way I see it, something has to break here. The equity on these miners are highly levered to gold prices. If gold stays flat or goes higher these stocks should move up.

Below is an illustration:

$2500 gold prices translates to about $231 on the GLD price. Buying the GLD January 2026 $235 strike price puts for $4.65 would put you in the money if gold falls below $2500 in 2025.

If gold falls to $2300 the GLD would fall to about $212. Your puts would jump to $17+ giving you a 281% return. You would end up with $17+ in total with a net profit of $12.35.

At $2300 gold prices IMG will generate about $450M based on their current guidance. That is a 7.5 multiple on the market cap at current prices. Not too shabby.

Endeavour mining will generate about $620M in profits. About the same multiple as IMG at 7.5.

If you simultaneously buy names like IMG and EDVMF and if gold drops to my hypothetical $2300 number you are still generating a 13%+ FCF yield on these names. So you make money from your short hedge in gold and your stocks still generate a very respectable FCF yield.

To limit your exposure even further you buy ITM 2026 leaps in gold names. I would buy in the money calls in this situation because that lowers risk and is my general preference. If the stocks are still cheap in a years time I would exercise the options and own the stock.

I used IMG as an example simply because I looked at the stock in more detail and built a position. But to lower company specific risks I would recommend buying a basket of longs including Iamgold, Endeavour, Newmont and maybe a gold miner index like the GDX or GDXJ.

Note that Newmont will generate about $3B at $2300 gold on a $47B market cap, which is about a 15-16 multiple. Not great but I would assume it will also get re-rated higher but the upside will be limited.

How should you size this position? A small 2% or less position in your portfolio through options seems about right for this approach because it is a trade for the most part. You could get a situation like last year where gold prices move or stay flat and the stocks are left behind which is a risk for this strategy. The market may just choose to ignore them for momentum names just as an example, you just don’t know in this market.

My overall position is higher simply because I built a position in IMG and am using this strategy to reduce some of my risk in the name. And as noted also added smaller positions in Newmont and Endeavour.

So the above gives you an idea of the pair trade.

Overall I like the risk/reward with this approach heading into 2025.